Context: a loss-making sheltered workshop wants to know which of its products and services generate profits or cause losses

The company had ample capital reserves and had been able to achieve positive annual results thanks to exceptional earnings, but its operations were loss-making. Although it was not my job as a director to make strategic and operational analyses, I organised strategic meetings with the directors and the entire management in order to give the organisation a clear direction.

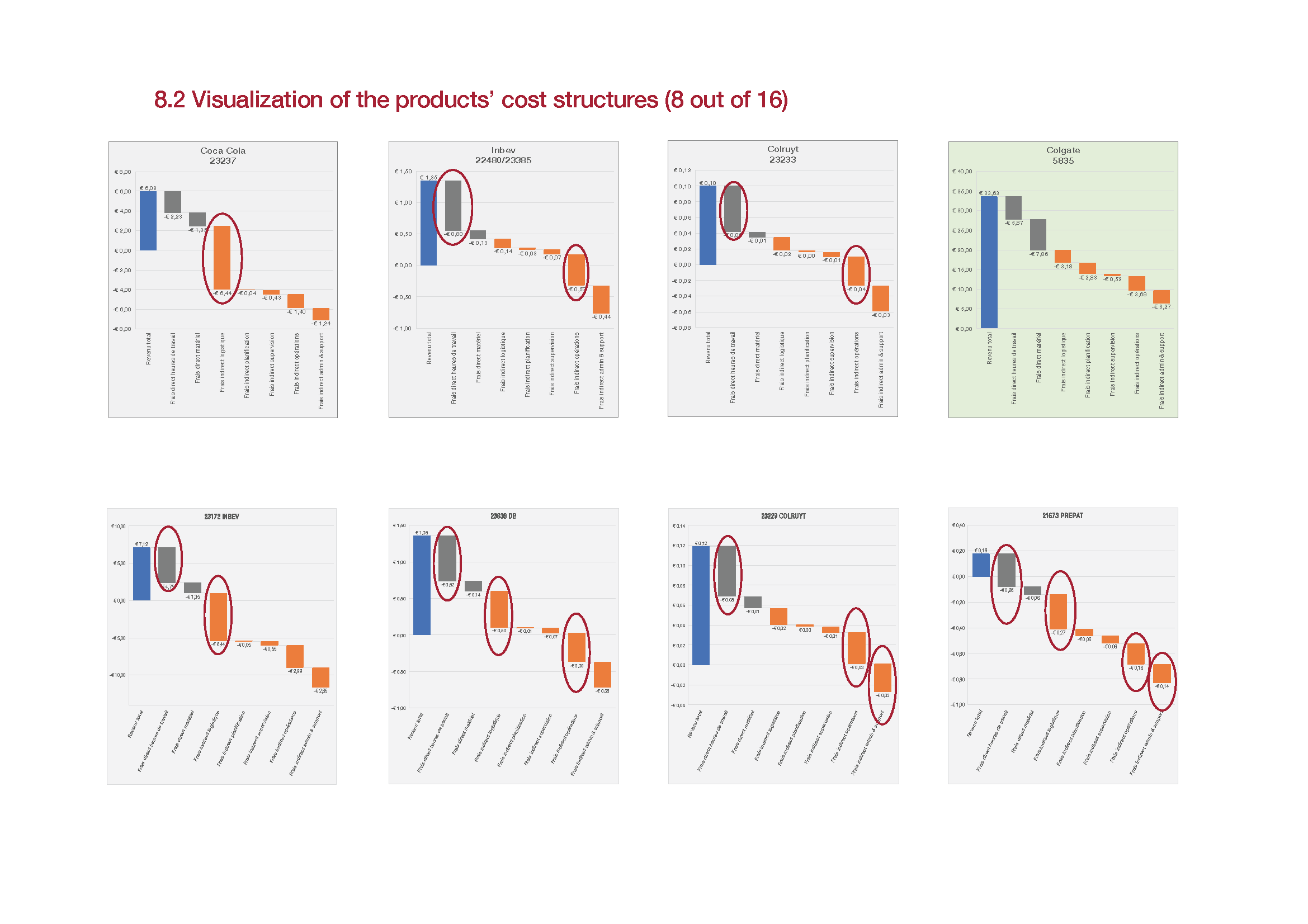

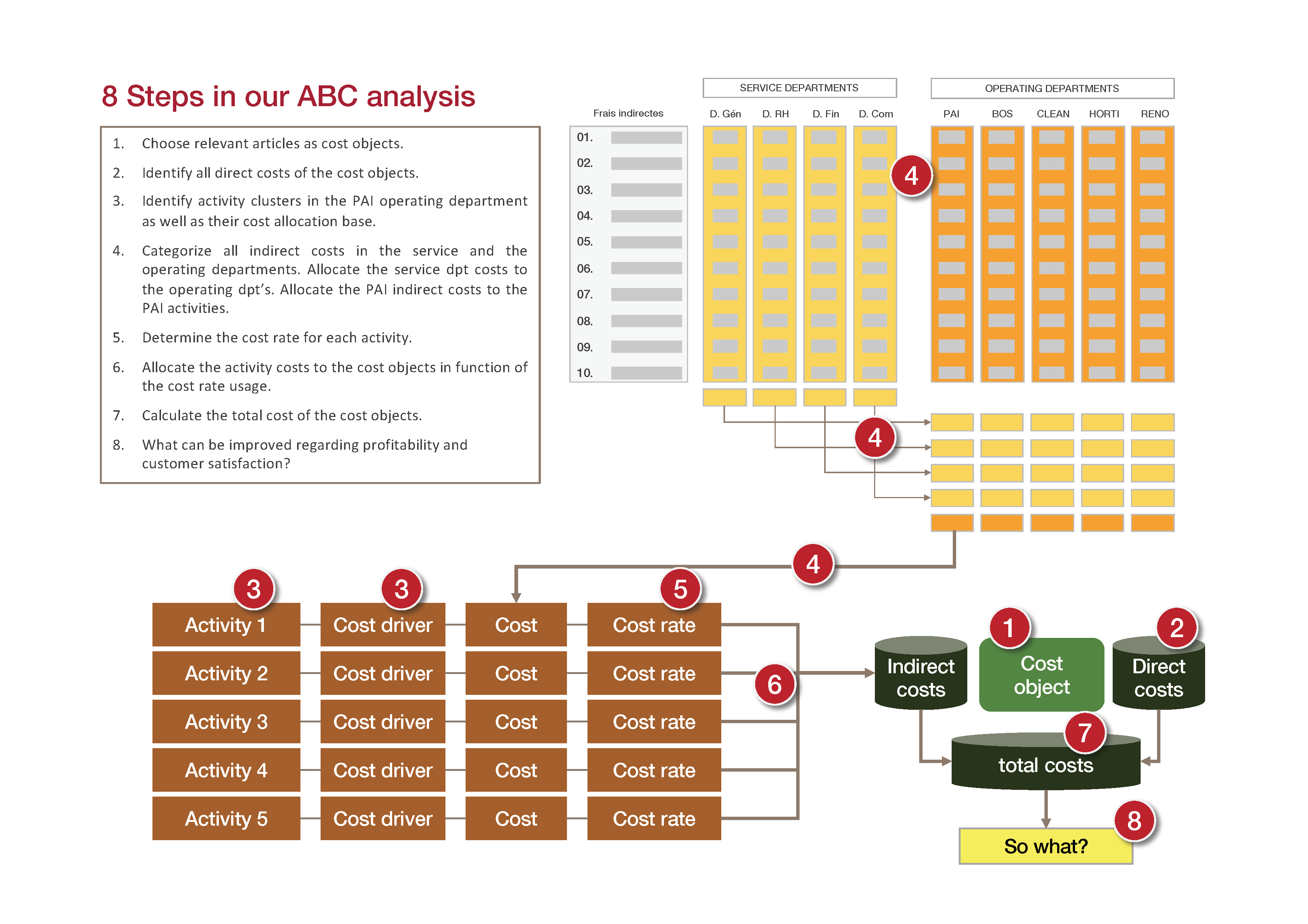

In this context an extensive Activity Based Management analysis was made of the assembly division in order to identify the products or services that generated profits or caused losses.

A methodology focusing on the accurate allocation of overheads.

A product or service first of all implies direct costs like the actual hours worked or the raw materials that were processed. In addition, there are overhead expenses for administration, sales, marketing, building, management, energy, etc.

These costs are “indirect” costs, as they cannot be linked to one specific product or service. However, these costs can be very high, which was the case here. Most companies use a relatively simple key, e.g. working hours per product, to allocate the indirect costs to a product.

The use of an incorrect key may have major consequences, as it may lead to an incorrect assessment of the actual costs, causing the management to make wrong strategic decisions that may have a major impact on the results of the company. The Activity Based Management (ABM) method, on the other hand, analyse the actual drivers of the indirect costs with a view to taking the right management decisions relating to product development, operations management and pricing on the basis of this information.

An analysis with far-reaching operational and strategic consequences

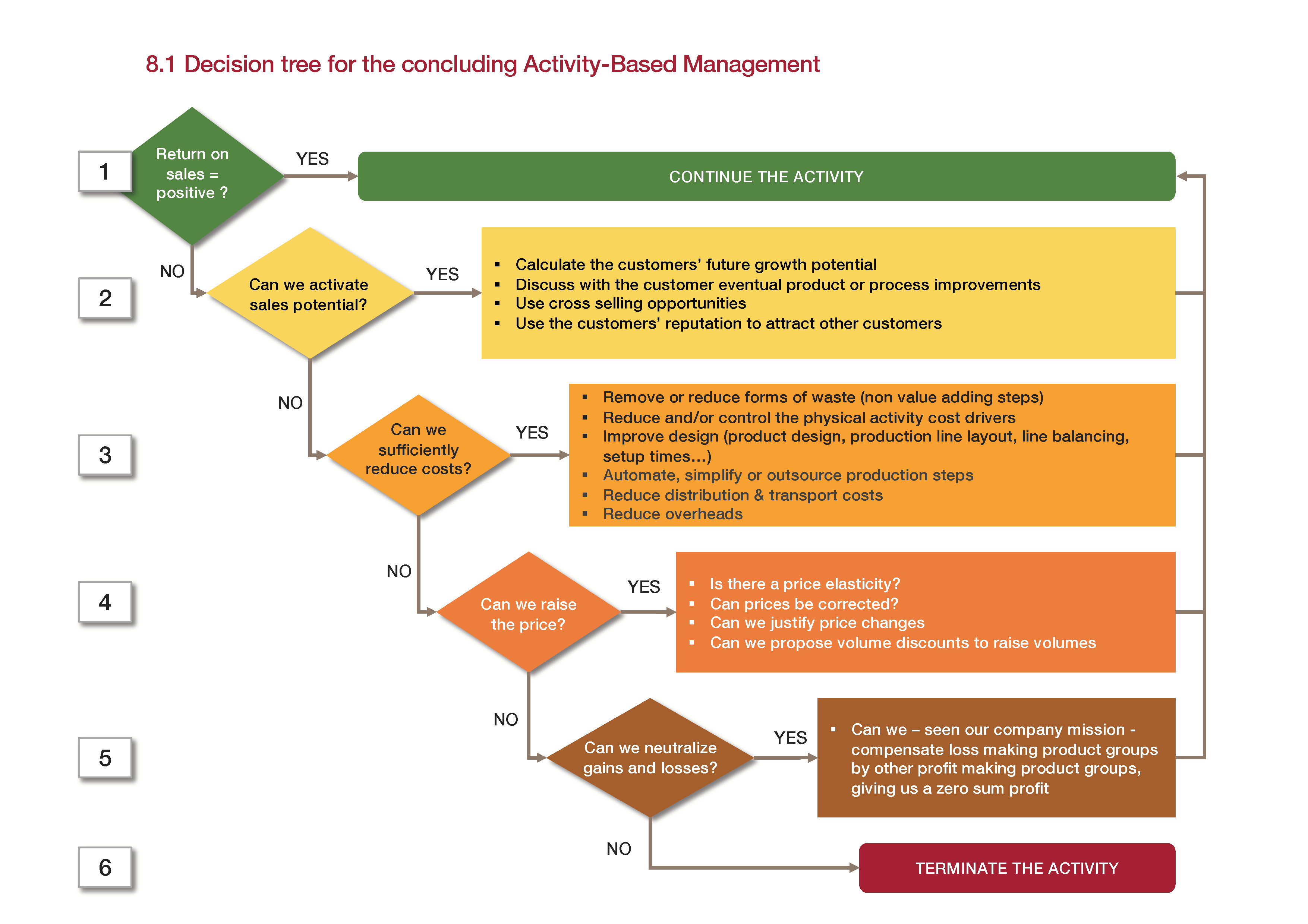

Once the margins of all assembly and packaging services offered were known, the further fate of a product or service could be determined. These are strategic decisions such as "continue the development of this product"; "look for larger volumes for this product"; "cut production costs"; "examine the price elasticity"; "accept the limited losses" or "stop this product".

The right strategic decisions can be made if the actual costs are known

Thanks to the ABM analysis, the management gained insight into the actual cost of its products and services and was better prepared to take decisions relating to pricing and production volumes.

As the sheltered workshop had excess production capacity and as the economic climate was favourable, one of the main conclusions was that costs should not be cut in the short term, but that investments had to be made in sales and marketing in order to increase production volumes. The following short-term and medium-term guidelines could be presented to the management:

1. Stop the bleeding.

The situation where the company was burning cash had to be stopped. The services generating heavy losses had to be cut back and new contract negotiations were supported by ABC simulations;

2. Increase sales volumes by investing in sales and marketing, in cross-selling, in product improvement and innovation...

3. Improve profitability in the medium term by working on process efficiency, by optimising the supply chain and by cutting indirect costs

4. Increase the prices of the products generating slight losses.